Financial institutions show increased appetite to lend to Polish real estate sector

According to a report by JLL, financial institutions are increasing the availability of real estate financing while the share of alternative lenders is growing. Retail real estate is the most favoured sector for financing. German banks remain the strongest players but Polish financial institutions have entered the race as well.

Warsaw, 8 June 2015 – International advisory firm JLL has prepared the report concerning real estate financing in Poland.

Piotr Piasecki, Head of Corporate Finance CEE, JLL, comments: “A full analysis of trends in terms of real estate financing cannot be properly performed without seeking the direct opinions of lending institutions. We therefore decided to interview representatives from 20 key market players, including banks and other financial institutions. The interviewees were asked about the level of interest in financing projects in Poland, the criteria for consideration, types of real estate that have the best chance of obtaining debt as well as alternative financing options and their achievable terms. This is the first report that analyses the condition of the real estate financing market in Poland on such a scale and complexity”.

Strong interest in financing

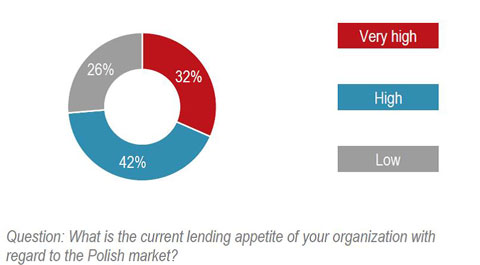

The survey conducted by JLL shows that there is strong interest from financial institutions in financing the Polish real estate sector: 74% of the people interviewed said that their organization has a high or very high lending appetite.

71% of participants offer debt financing, while 29% are willing and ready to finance other parts of the capital stack (including mezzanine, financial or operating leasing). 69% offer both investment and development loans.

Despite the attractive terms and decreasing costs of financing, lenders continue to be cautious and the majority of them require a full security package (standard guarantees, full hedging, soft and hard covenants).

Criteria for considering real estate financing- location and asset quality

“Lending institutions put a greatest emphasis on the location and the quality of an asset when considering real estate financing. However, factors such as the leasing status of the property, the occupancy level and WAULT, a developer’s or investor’s reputation, their level of equity and the business situation of the borrower play secondary but still important roles. What is worth noting is the fact that the least significant consideration for lenders, provided that other criteria are satisfied, is the actual size of the loan”, claims Piotr Piasecki.

Development loans – appetite for retail projects

The openness to development financing in Poland is emphasized by the wide range of attractive terms offered to developers. Borrowers can apply for loans at the level of 60% – 80% LTC[1] on attractive margins of 200 – 300 bps. Lenders’ demands for pre-let level vary from 40% to 60%.

Anna Grzędzińska, Consultant, Corporate Finance CEE at JLL, comments: “Research shows that among all sectors of the commercial real estate market, retail projects were the most preferred asset class for development financing. What is more, the lenders are open to the financing of both prime and prime – value added products in this sector. Furthermore, office projects and industrial projects, enjoy interest as well. Opportunistic assets, especially from the office and retail sectors, are mainly on the radar of alternative lenders, who are keen to take on more risk in return for higher profits.”

Investment loans

The results of the survey show that investors can obtain very favourable terms, which is especially reflected in the downward pressure on margins. The vast majority of the surveyed organizations provide financing of up to 70% LTV[2] with attractive margins at 200 - 300 bps or even less. However, it should be stressed that the organizations which gave this answer will, on the whole, not go lower than 150 bps.

Similarly to development loans, lenders are willing to finance mainly prime retail assets (95% of responses). They are closely followed by prime warehouse and office projects. The prime – value added office and retail class assets are also deemed attractive.

“The trust in the retail real estate segment stems from several factors, including good economic conditions, growing consumption and an increase in purchasing power combined with interest from investors. It is also worth noting that margins on retail projects are slightly higher than on office projects and, therefore, financing them is more profitable for lenders,” adds Anna Grzędzińska.

The real estate financing market – downward pressure on margins, dominance of German banks

In recent years, prime margins offered by financial institutions on the Polish market have steadily fallen from their recession highs (from 325 bps in 2010 to 150 – 175 bps in 2015 for prime commercial assets). All-in cost of finance remains low throughout Europe, particularly for German-based lenders which have access to cheaper euros through Pfandbriefs and Landesbanks.

“German banks are still the strongest players on the Polish market. Their ability to offer cheap long-term financing gives these banks a significant advantage over their Polish counterparts. Nevertheless, we observe that Polish financial institutions are closely watching the trends and trying to successfully compete with German institutions,” explains Piotr Piasecki.

The significant improvements in the financial terms offered by banks coincided with new lenders, including non-banking institutions, entering the market and actively seeking new opportunities. As a result, a wide range of financing terms and structures are now available.

Investment market and access to financing

The Polish economy remains resilient, despite recent tensions between Russia and Ukraine as well as deflation, which is still on the rise. According to Consensus Economics, GDP growth in 2014 was 3.3% (y-o-y). Furthermore, 2015 shows a positive picture of the Polish economy. Solid fundamentals are underpinned by the on-going recovery of the European economy, which has led to lenders and investors remaining optimistic with regard to the Polish commercial real estate market's prospects in the near future.

Tomasz Trzósło, Managing Director, Head of Capital Markets Poland, JLL, summarizes: “Investors’ appetite for Poland remains strong across all asset classes and sectors. Attractive and easily-achievable financing widens the pool of investors who are able to offer more competitive pricing. This is especially the case for sources of capital which previously looked only at opportunistic product. Nowadays, they can achieve healthy results on less aggressive assumptions on rental growth and/or yield compression.”

[1] LTC (Loan-to-Cost) – relation between the amount of loan and the cost of the investment

[2] LTV (Loan-to-Value) – relations between the amount of loan and the asset’s value