2010 saw a recovery in the regional Polish office markets. Prime office headline rents have stabilized and corporate demand for office space started to recover.

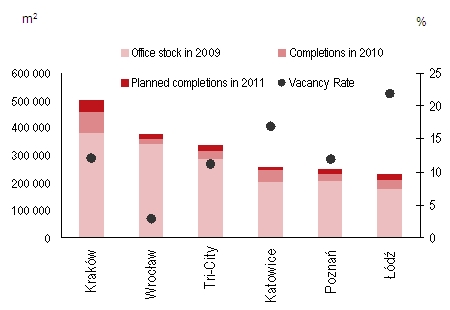

Warsaw, 31 January 2011 - The total modern office stock in the key regional markets of Poland (i.e. Kraków, Wrocław, Katowice, Poznań, Tri-City and Łódź) was 1,820,000 m², of which the office stock located in Kraków and Wrocław represents 45% of the office stock as above.

Approximately 215,000 m² of new office space was added to the markets listed above, which is comparable to 2009 with around 227,000 m² coming to the market. 29,000m² of new office space was delivered to the market in Q4 2010, mainly in Lodz (Sterlinga Business Center) and Poznan (Malta Office E). Another 140,000 m² are set for completion this year with the biggest being Bonarka 4 Business A&B (16,000 m²) in Kraków, Oliva Gate (15,900 m²) in Gdańsk, Park Biznesu Teofilów I (8,500 m²) in Łódź and Wojdyła Business Park II (7,700 m²) in Wrocław.

Mateusz Polkowski, Senior Research Analyst, Jones Lang LaSalle said: “We noticed an increase in corporate demand in all major office markets over 2010. 230,000 m² was leased in regional markets, with Kraków and Wrocław clearly taking a lead in respect of occupier activity. Take-up was generated by both newcomers (e.g. IBM in Wrocław, Sony in Tri-city) and expanding companies already operating in these cities (e.g. Motorola or Capgemini in Kraków).”

Office buildings totaling 238,000 m² were under construction across major regional office markets, with construction activity most pronounced in Wrocław, Kraków and Tri-City (62,000 m², 55,000 m² and 42,500 m² respectively). This excludes a variety of projects whose construction started and was subsequently put on hold which represent another 69,000 m². The biggest office projects being currently developed in Poland include: Sky Tower in Wrocław, Andersia Business Centre in Poznań and Oliva Gate in Gdańsk.

New, “secondary” office locations in Poland (i.e. Szczecin, Lublin, Rzeszów, Bydgoszcz, Toruń, Olsztyn, Białystok and Kielce) are also pro-active in respect of preparing office accommodation for occupiers, most notably BPO and SSC type of tenants. The first true modern office building in Szczecin, namely Oxygen (14,000 m²), was completed by Echo Investment in H2 2010.

As at the end of 2010 vacancy rates remained stable in Wrocław, Tri-City and Katowice (averaging 2.8%, 11.2% and 16.8% vs. 3.2%, 11.0% and 17.0% in Q3 2010, respectively). Slight upward pressures were registered in Kraków, Łódź and Poznań with a vacancy rate at 12.1%, 21.8% and 11.9% in Q4 2010, up from 10.7%, 20.0% and 8.0% in Q3 2010 respectively. The slight increase resulted from a delivery of new office buildings in 2010, which to a great extent remained vacant: Vinci Office Center in Kraków, Francuska Office Centre A & B in Katowice, Sterlinga Business Center and University Business Park I in Łódź.

The office vacancy in Poland ranging in most markets between 10-20% provides a reasonable choice of accommodation for office occupiers, an important factor for BPO and SSC centres amongst others. Wrocław with a vacancy ratio of less than 3% is unique in this respect, and this undersupply of office space triggers new development on this market. Major pipeline office provision includes: Green Towers I, Sky Tower and Wojdyła Business Park phase II.

Prime headline rents currently range from €11-13.5 /m²/ month in Łódź, to €15 /m²/ month in Kraków, Wrocław and Poznań. We expect slight upward pressures on the headline rents in 2011 in most regional markets.

Modern Office Stock and Vacancy Rates

(as at the end of Q4 2010)