Modern office stock and vacancy rates

(as at the end of Q1 2011)

Source: Jones Lang LaSalle, Q1 2011

Rental growth possible going forward

Warsaw, 19th April 2011 - 2010 saw a recovery in the regional Polish office markets. Prime office headline rents have stabilized and corporate demand for office space started to recover. This trend continued in the first three months of 2011.

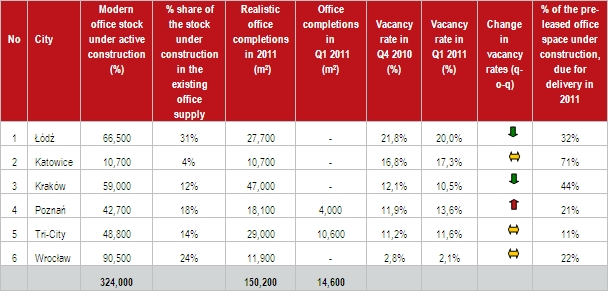

As at the end of Q1 2011 vacancy rates remained stable in Wrocław, Tri-City and Katowice (averaging respectively 2.1%, 11.6% and 17.3% vs. 2.8%, 11.2% and 16.8% in Q4 2010). Slight downward pressures were registered in Krakow (from 12.1% to 10.5% q-o-q) and Łodz (from 21.8% to 20%).The increase in vacancy level affected Poznań only with vacancy rate now at 13.6%, up from 11.9% in Q4 2010. The minor growth resulted from a delivery of two office projects, which to a large extent remained vacant.

Currently the pre-let status in the office stock under active construction ranges between 11% in Tri-City to 71% in Katowice. It effectively means that approximately 85.000 m2 of the modern office stock due to enter the regional markets over 2011-2012 remain unoccupied.

Anna Bartoszewicz-Wnuk, Head of Reasearch & Consulting at Jones Lang LaSalle comments: „An improvement to the corporate demand in all major office markets (over 230.000 m2 leased in 2010) translated into new office start-ups. Currently around 324.000 m2 of office space remain under active construction across Poland - majority of which in Wrocław (over 90.000 m2) and Łódź (around 66.000 m2), where the office space under construction is equal to around 25 and 30% of the existing office space supply on these markets respectively. Katowice is on the other end of the construction activity scale with just 10.700 m2 at the construction stage.”

2011 will see a completion of around half of the office supply under construction. According to Jones Lang LaSalle’s estimates, 135.000 m2 of the speculative modern office space will realistically enter the regional markets over Q2-Q4 2011, in addition to 14.600 m2 completed in Q1 2011. This effectively means that the new supply is slowing (a 34 and 31% decline on 2009 and 2010 figures respectively). Major pipeline office provision for 2011 includes: Bonarka 4 Business (buildings A and B of a total office area of around16.000 m2) and Green Office (buildings A and B of the total office area of around 11.000 m2), both located in Kraków, as well as Olivia Business Centre in Gdansk (the first building in the complex - Olivia Gate - offering approximately 15.900 m2)”.

„Taking into consideration the availability of the existing office area, the pipeline office supply for 2011 and the improving economic indicators, there is increasing confidence that the recovery trend will continue and filter into new start-ups of projects put on hold during the market slowdown.” – adds Anna Bartoszewicz-Wnuk.

Prime headline rents currently range from €11-13.5 /m2/ month in Łódź, to €15 /m2/ month in Kraków, Wrocław and Poznań. Prime headline rents are likely to remain stable throughout Q2 2011, with slight upward pressures anticipated in H2 2011 in some of the regional markets.